What Does War Do To the Stock Market? Should You Worry?

The Russia-Ukraine conflict has left many investors worried as they wonder what will happen to their stocks during the war. That is why it is especially important during times of heightened volatility and uncertainty to remember the fundamentals of investing and the keys to mastering behavioral finance.

Waking up to the news that Russia and Vladimir Putin had launched a devasting attack on Ukraine was unsettling, to say the least. Of course, this came after weeks of speculation that this sort of event might happen, but the shock was ever present. Immediately, fear and uncertainty began to sweep through the news cycle, or should I say continued. Since February of 2020 and the onset of the COVID-19 pandemic, fear and uncertainty have dominated the media narrative, even more than usual.

At a time when there are so many innocent lives at risk, it may seem trivial to discuss something as temporal as money. But, we also know that our financial lives greatly impact the rest of our lives. And, since I’m no geopolitical expert, I’ll keep the focus of this post to what I do know.

So, Should You Worry About Stocks During a War?

Well, as I work my way toward an answer, perhaps I can pose a question to the question? Does the occurrence of any event mean you should worry? The debate over this could rage on, I’m sure, but I’m in the camp that believes worrying, by itself, will not help protect you from what you’re worried about.

Most things we worry about are things that are out of our control? Why? We’re human and we like control. It’s no secret that there are many things in our lives that are out of our control. Those things may provide good opportunities to worry, but should we worry about any of them? I can’t see how doing so would help the situation.

It’s also important to understand that the advice, “Don’t worry” doesn’t mean don’t plan. In fact, it’s quite the contrary. While there are many things out of our control, there are also some things that are in our control. In your financial life, or your life in general, taking prudent action to plan and address possible risks is not only well-advised, it’s imperative!

So, should you worry about the war or worry about what your stocks will do during the war? Well, no.

Does War Mean Make Changes?

Whether warranted or not, many investors made changes as a result of the Russia/Ukraine conflict. According to Alight Solutions, 401(k) investors have reacted to the news in a big way, driving higher than normal trading activities. In the days leading up to the beginning of the Russian invasion, Alight cited that trading activity had increased to as high as 7.5 times normal levels. As during other volatile periods, they also saw investors were moving out of equities (stocks) and into fixed income (bonds).

I get it. Investing in stocks during a war is scary. This activity is evidence that many investors are making important decisions that have long-term implications based on the short-term news cycle. In other words, many investors continue to try and “time the market,” something that some of the most established names in finance say is nearly impossible. Whether the motivator is fear or greed, neither can change the strong evidence against market timing as an effective, long-term investment strategy.

In short, market timing usually leads to missing out on gains while waiting for a downturn. For example, if you look at what happened to the S&P 500 on February 24th and 25th, you’ll see a good example of what often happens when implementing a market timing strategy.

If you sold near the market open, when the S&P 500 hit its low for the day around $4,136.53, you would have actually missed out on nearly a 6% rebound that took place by the end of the week. When that happens, investors are faced with a more difficult question; “Should I get back in now and concede the 6% or should I wait and hope the market comes back to where it was so I can buy back in?” The consequences of waiting could prove increasingly detrimental, as the market could continue to rise.

In fact, we saw this happen in 2020. If you sold near the bottom of the decline, when the S&P 500 was approximately at $2,304 with the notion that it was going to go lower, you’d still be waiting for that to happen (missing out on over a 90% increase as of March 4, 2022).

What Should You Do?

If worrying, reacting, and panicking is not recommended, what is? Having a financial plan before a crisis is obviously preferred, although this is clearly not always the case. However, if you find yourself in a crisis without a financial plan, it’s not too late to get one. Seeking help from a CERTIFIED FINANCIAL PLANNER™ professional is a good place to start.

But, what if you already have a financial plan? If you have a plan, and if it’s a good one, then the answer is simple; stick to your plan. However, this may be simple, but certainly not always easy.

Crisis situations and the media headlines that follow will often imply or create the notion that you, as an investor, should be “doing something.” It can almost feel irresponsible to do nothing during these times. But, often times, nothing is exactly what you should be doing (assuming your plan was good to begin with).

Let’s be honest. Should any prudent financial plan require a regular, everyday investor to adequately navigate the aggregate of complex risks like inflation, geopolitical risks, domestic political concerns, market valuations, COVID-19, and the Fed talking about raising interest rates? If any plan does, then it is a bad plan. Not even the brightest financial professionals can consistently predict the short-term direction of the stock market and how it might react to these types of issues.

No, a good plan addresses short-term and mid-term risks, but it also needs to address the long-term as well. A good plan likely involves proactive, up-front moves that hedge these many risks, followed by extreme discipline over the long-term to not deviate from your strategy.

The problem is that some investors will completely lose sight of the long-term during a short-term crisis. This causes some to make knee-jerk investment decisions. And, who’s perpetuating these feelings and poor decisions; none other than the financial media.

As mentioned above, there were multiple outlets in March of, 2020, after the S&P 500 had taken a 33% dive, that suggested the market would decline yet another 30%-35%. But, after the S&P 500 roared back and increased over 90% thereafter, did that hurt the financial media outlets making these ominous predictions? No. But, did it hurt investors? Yes, it assuredly did.

That is the problem. The financial media is not incentivized to help investors make better decisions and improve their returns. They are incentivized to drive ratings and stir up emotions. There is no better emotion to stir up than fear. That same fear, though, is often what causes everyday investors to make poor decisions. Those same poor decisions can create insurmountable hurdles for the average investor struggling to save enough for retirement.

Generally Bad Reasons to Make Investment Changes

With these thoughts in mind, is there ever a good reason to make a change to your investment strategy? Of course. But, those reasons should generally be because something has changed in your life. For example, perhaps you decided to retire sooner, received an inheritance, or had a major expense arise. These are all potential reasons to adjust your strategy.

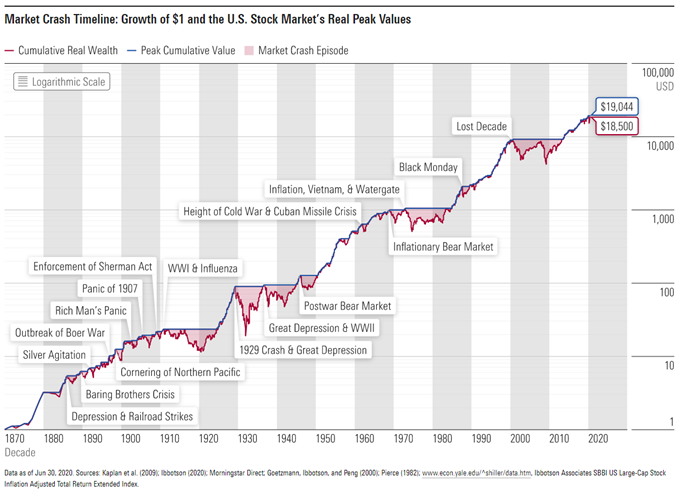

But, making changes to your long-term investment strategy based on short-term headlines (i.e. geopolitical issues like Russia and Ukraine) is usually not advised. These types of things will continue to happen, but they’re impossible to predict. The stock market, however, has taken these events in stride decade after decade, crisis after crisis.

Bottom Line

War, and other major world events (like the COVID-19 pandemic) can be scary. They increase uncertainty and can also cause investors to worry. However, that doesn’t mean you should automatically worry about what will happen to your stocks during a war.

At all times, and in every environment, you need to be sure you have a sound financial plan to lean on. If you don’t have one, get one. If you have one, stick to it. Changes and adjustments are likely to be needed at some point, but should likely be made as a result of changes in your situation, not changes to things you cannot control.

Keep your focus on controlling what is in your control. And, when it comes to managing your emotions in a crisis, it may suit you best to turn off your television and avoid viewing your portfolio balances every day. Avoiding these things can help reduce your financial anxiety.

Lastly, if the volatility of the market is too much for you to handle, outsourcing your investment management to a professional may be the best route for you. Not having a good advisor in a crisis is like an airplane passenger trying to perform an emergency landing with no pilot and no guidance. If it were up to me, I’d rather stay in the back while the pilot completes a smooth landing.

For more information or a review of your financial plan, contact us at 618-288-9505.

Joe Allaria, CFP®

Wealth Advisor | Partner

Follow me on Social Media

Free Retirement Assessment

Our free assessment will show you how to invest confidently, reduce taxes, and retire successfully. We want you to know exactly how we can help before you pay us a single dollar.